I &M Bank Ranked the strongest bank in Kenya

I &M Bank Ranked the strongest bank in Kenya

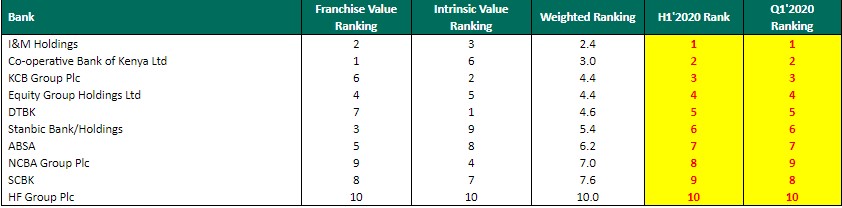

Cytonn Investments has today released its H1’2020 Banking Sector Report, which ranks I&M Holdings as the most attractive bank in Kenya, supported by a strong franchise value and intrinsic value score. The franchise score measures the broad and comprehensive business strength of a bank across 13 different metrics, while the intrinsic score measures the investment return potential.

The report, themed “Depressed Earnings and Deteriorating Asset Quality amid the COVID-19 Operating Environment,” analysed the H1’2020 results of the listed banks. “Asset quality for listed banks deteriorated in H1’2020 with the Gross NPL ratio rising by 1.6% points to 11.6% from 10.0% in H1’2019. This was high compared to the 5-year average of 8.5%. Consequently this led to increased provisioning across the industry to proactively manage risks given the tough economic conditions, which saw the NPL coverage rising to 57.8% in H1’2020 from 55.9% recorded in H1’2019. In accordance with IFRS 9, banks are expected to provide both for the incurred and expected credit losses. We expect higher provisional requirements to subdue profitability during the year across the banking sector on account of the tough business environment”, said David Gitau, Investment Analyst at Cytonn Investments. Five key drivers shaped the Banking sector in H1’2020, namely Regulation, Monetary Policy, Consolidation, Asset Quality, and Capital Conservation.

“On the regulatory front, The Central Bank of Kenya on March 27th, 2020 provided commercial banks and mortgage finance companies with guidelines on loan reclassification, and provisioning of extended and restructured loans as per the Banking Circular No 3 of 2020. The Central Bank stipulated that banks would be allowed to extend loan repayments for their customers for a period not more than one year, the cost of restructuring and extension of loans would be met by the banks and they would have to report any restructuring in relation to the COVID-19 pandemic to the Central Bank monthly. According to data from the July 2020 Monetary Policy Committee (MPC) Meeting, this has seen a total of Kshs 844.0 bn, representing 29.1% of the total Kshs 2.9 tn banking sector loan book, being restructured as at June 2020”, said Ann Wacera, an Analyst at Cytonn Investments.

III. Average loan growth came in at 14.5%, which was faster than the 9.8% recorded in H1’2019, but slower than the 25.9% growth in government securities, an indication of the banks preference of investing in Government securities compared to lending to individuals and businesses,

IV. Interest income rose by 10.4%, compared to a growth of 3.7% recorded in H1’2019. The faster growth in interest income may be attributable to the 16.1% growth in loans and increased allocation to government securities. Despite the rise in interest income, the Yield on Interest Earning Assets (YIEA) declined to 9.7% from the 10.4% recorded in H1’2019, an indication of the increased allocation to lower-yielding government securities by the sector. The decline in the YIEA can also be attributed to the reduced lending rates for customers by the sector, in line with the Central Bank Rate cuts. Consequently, the Net Interest Margin (NIM) now stands at 7.0%, compared to the 7.7% recorded in H1’2019 for the listed banking sector, and,

V. Non-Funded Income declined by 1.1% y/y, slower than 16.5% growth recorded in H1’2019. The performance in NFI was on the back of declined growth in fees and commission of 3.4%, which was slower than the 12.7% growth recorded in H1’2019. The low growth in fees and commission can be attributed to the recent waiver on fees on mobile transactions below Kshs 1,000 and the free bank-mobile money transfer. Banks with a large customer base who rely heavily on mo